Or “creditworthy or not creditworthy,” that is the Schufa Simulator question

Schufa—a term well known to many people in Germany. Especially in consumer transactions, nothing works without Schufa anymore.

But how does this mysterious institution actually work? And what can we learn from the new Schufa Simulator?

In this blog post, we get to the bottom of how Schufa works and shed some light on the darkness of the rating process. It’s going to be exciting!

We would probably all like to have this rating

Schufa: A look behind the scenes

Schufa, or the Schutzgemeinschaft für allgemeine Kreditsicherung, is a private credit bureau that assesses the creditworthiness of consumers. It collects information on financial activities such as loans, payment behavior, ongoing contracts, and more. This information is used to create a credit score, which is used by banks, landlords, and other companies for risk assessment.

The Schufa assessment is based on data reported by contractual partners. Positive behavior, such as punctual payments, leads to a better rating, while negative factors, such as payment delays or insolvencies, can worsen the rating. Schufa itself does not issue grades, but merely provides information that companies can use to make their own decisions.

Until now, the Schufa score was the ominous Sword of Damocles or, as shown here, the “Damocles Chainsaw” that hung over us all.

The rating is where it already becomes problematic

Always be the first to receive the latest news, interviews, and expert articles?

The Schufa Simulator: Slightly more transparency than before

The new Schufa Simulator promises more transparency and understanding for consumers. It allows people to simulate their individual creditworthiness and understand the effects of certain behaviors. This can be a valuable aid in personal financial planning.

https://www.schufa.de/scorechecktools/pt-scoresimulator.html#0

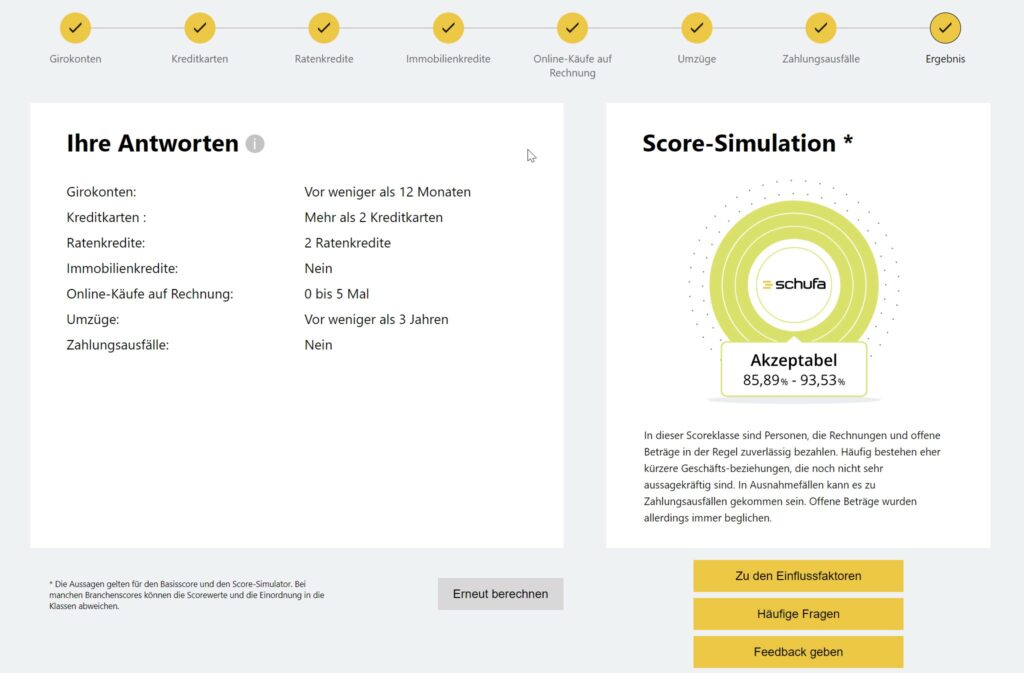

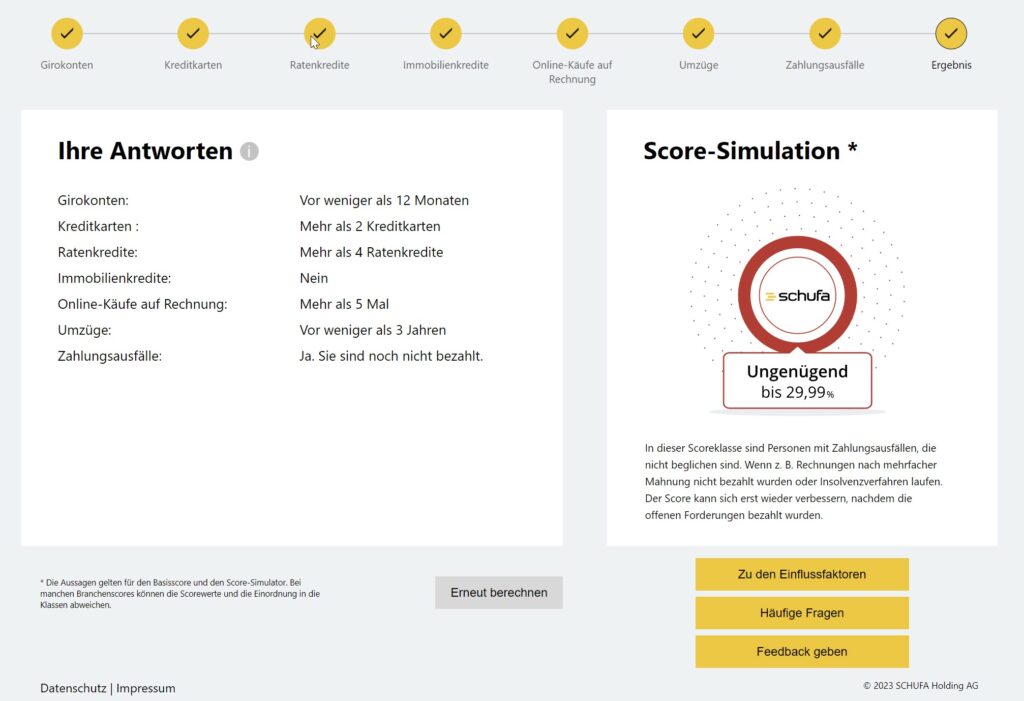

With the Schufa Simulator, users can simulate scenarios of how certain financial decisions might affect their Schufa rating. For example, one could test how opening a new credit card, taking out an installment loan, or delaying payment on an invoice would affect their Schufa score. This type of insight can help in making informed decisions and specifically improving one’s own financial behavior.

Insights from the Schufa Simulator: Unfortunately, the Schufa Simulator only provides us with rudimentary insights

Understanding correlations: By playing through various scenarios, we can better understand how our financial decisions can influence our creditworthiness. This knowledge can help to avoid ill-considered actions.

Long-term planning: Through simulation, we can recognize the effects of long-term financial strategies. This is particularly helpful when planning major financial projects such as buying a property or starting a business.

Early identification of problems: The Schufa Simulator can point out potential weaknesses in our financial behavior before they become serious problems. This allows us to take corrective action in good time.

Optimization of creditworthiness: By specifically simulating positive actions, we can find out how to improve our creditworthiness. This can secure better conditions for loans and contracts in the future.

And this is where everything stops working

BUT, and here is the catch:

The very simple and few parameters shown here are not everything that happens in the background. Many data points are not available at all and are therefore not taken into account, such as:

Income in relation to expenses, loans, etc. Someone who earns €150,000 a year and, for whatever reason, has 5 installment loans with €100 monthly repayments will be rated worse simply because of the number of loans. For someone who only earns €20,000 a year, I would understand that more. Or do they have access to data provided by the tax office?

The duration of installment loans. This is stored in the real system, but not in the simulator.

Will someone who pays off €10,000 in 12 installments be rated just as poorly as someone who does it in 48 installments? Who is better and why?

Those who move often, lose out. If you work in the military or another organization that makes you move every 2 years and perhaps even pays for it, then that should probably be assessed differently than if someone is kicked out of their apartment every 2 years and moves because of it, or regularly has such increases in income. Here, however, it seems to depend only on the raw number.

The number of credit cards is to be assessed similarly to installment loans. I also have several credit cards. But I also have 2 businesses, so that’s 2 cards for those alone. And as a partnership, these go on my “private rating.” Together with my private credit cards, I am immediately put into a category of consumers who apparently need many credit cards just to be able to pay for anything at all. Whether there is any turnover on these cards at all or whether installment payments have been agreed upon is not something I see as a criterion here in the simulator either.

Home or apartment ownership also has a positive effect. However, there is probably no difference whether the high earner, who easily shoulders the monthly credit installment, is rated the same as the family where both spouses work, one even has a side job, and they save on food and vacations to afford the installments.

Because what comes next, but in secret?

In the USA, behavior on social media platforms is apparently already being included in the calculation of creditworthiness. I will research that first.

Where does it all end? In a social credit system in “Chinese fashion.” If any of us would like that, please shout “Here” loudly!

A future that nobody actually wants. More on this soon in a new blog post.

Conclusion: For those who “simulate” here, transparency is merely an illusion!

The Schufa Simulator does offer a way to better understand how Schufa works and simultaneously optimize our own financial behavior. However, the relevant “levers” cannot be grasped by the end user at all.

This creates an illusion of transparency for the consumer and addresses the eternal question of “how do they actually calculate that?” What is really going on cannot be recognized at all. The Schufa Simulator is therefore just window dressing to make one feel more informed and, ultimately, a marketing tool rather than a transparency instrument. A shame, really.

If you like my articles and would like a critical digitalization consultant in your project who advises you objectively and neutrally, then simply schedule a free initial appointment with me.

Schufa turns the “blind” into the “one-eyed,” but not into those who “see”

Image sources: Shutterstock and Schufa